Overnight Interest Rate and REPO Operations

In the complex and fast-paced world of financial markets, liquidity is the lifeblood that ensures smooth operation. One of the critical tools central banks and financial institutions use to manage liquidity and stabilize markets is the repurchase agreement operation, commonly referred to as REPO. This mechanism plays a pivotal role in influencing overnight interest rates, ensuring that short-term borrowing and lending needs are met efficiently.

The rate at which banks and institutions lend and borrow short-term money through these REPOs is called the “overnight interest rate”. Central banks set this rate as a primary tool to influence monetary policy and economic activity. Changes in the overnight rate ripple through the economy, affecting borrowing costs for businesses and consumers, inflation levels, and overall economic growth.

In this article, we will delve into the concept of REPO operations, exploring how they function, their significance in the financial system, and the potential risks they carry.

What is a repurchase agreement operation?

A repurchase agreement operation (REPO) is a short-term financial transaction primarily used by institutions to borrow or lend money in exchange for interest for a short period (usually overnight or for a few days).

It involves the sale of securities with an agreement to repurchase them at a specified future date and price. Essentially, a REPO functions as a collateralized loan where the securities act as collateral to secure the transaction.

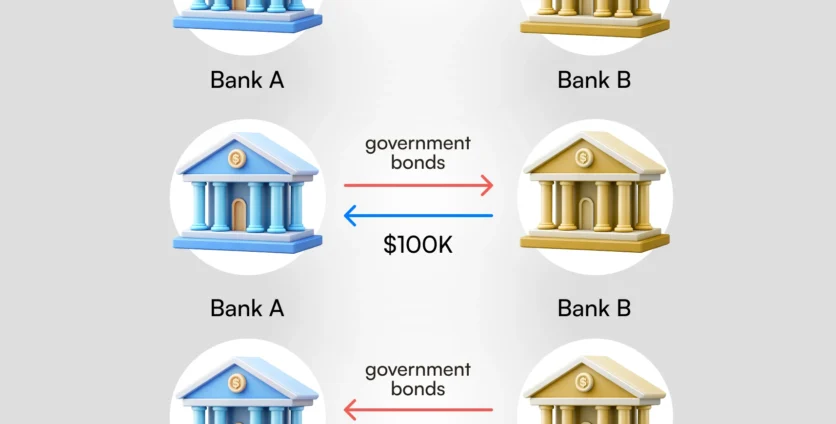

How does a REPO work?

Imagine a situation where Bank A, for some reason, experiences an immediate need for cash. It does not have all the necessary funds at the moment, so it asks Bank B to lend the necessary amount.

To do that, Bank A sells Bank B government debt securities for $100K, signing an agreement to repurchase the securities at a higher price, basically paying interest for the borrowing. Let’s assume the overnight interest rate of the Central Bank is 5%. As a result, Bank A must pay $105K to Bank B when repurchasing the securities. In case Bank A defaults during this period, Bank B can keep the purchased securities as collateral to shield itself from counterparty losses.

The difference between the sale and repurchase prices represents the REPO rate, which is effectively an overnight interest rate for the transaction.

Central banks conduct REPO operations to regulate liquidity levels in the market. For instance, during periods of tight liquidity, a central bank might inject funds into the system through REPO transactions, allowing banks to meet short-term funding needs. Conversely, reverse REPO operations allow central banks to absorb excess liquidity by selling securities with an agreement to buy them back later.

What are the risks of REPO?

While REPO operations are integral to maintaining liquidity and stability in financial markets, they are not without risks. Understanding these risks is crucial for both participants and uninvolved third parties.

- Counterparty risk. The primary risk in a REPO transaction is counterparty risk, meaning the possibility that one party might default on their obligation. If the borrower fails to repurchase the securities, the lender may face losses despite holding collateral.

- Market risk. The value of the collateral can fluctuate due to changes in market conditions. If the value of the securities declines significantly, the lender may find it challenging to recover the full loan amount in the event of default.

- Liquidity risk. In stressed market conditions, even high-quality collateral may become difficult to sell, potentially exacerbating financial instability.

- Systemic risk. The interconnectedness of financial institutions through REPO markets can amplify systemic risk. A significant disruption in the REPO market can have cascading effects on the broader financial system, as seen during the 2008 financial crisis.

To mitigate these risks, participants often use “haircuts” — a discount between the market value of the collateral and the amount lent — to provide a buffer against potential losses.

Regulatory measures, such as capital requirements and stress testing, also aim to ensure the resilience of REPO markets.

Conclusion

Repurchase agreement operations are a cornerstone of modern financial systems, providing essential short-term liquidity to banks, financial institutions, and central banks. By influencing overnight interest rates, REPO operations help maintain stability and ensure the smooth functioning of money markets.

Discover the latest Headway updates on Telegram, Facebook, and Instagram.